First, I’m sensing a fair amount of competitiveness (my investing karate is better than your investing karate – drops mic)…my hope is that we work collaboratively to improve everyone’s outcome.

Hi Ricky Spanish

Admittedly, I didn’t read the links you posted. No offense, it’s just that I studied investing options intensely long ago, developed a plan based on what I learned, and have stuck to my plan ever since. Pilots are taught to “plan your flight – fly your plan” and that’s exactly what I’ve done. Just so you know, I’m 52, I’ve been flying my plan since my divorce at 29, and despite setting an ambitious financial goal for myself, I’m significantly ahead of plan.

I did notice that two of your article titles mentioned “good financial advisors”. Well, that pretty much kills it right there…you don’t get to cherry pick after the fact; come on.

BTW, have you ever heard commercials where they say something like “90% of our funds have outperformed their respective Lipper averages over the last XYZ years” Yah, they systematically drop their poorly performing funds and then only include currently available funds in the calculations…that’s called selection bias and you can produce any statistic you want if you’re willing to stoop to that level.

You Wrote: MS wants to have funds which they can manage, and grow, so they can, you know, make more money since they're paid off the value of the account.

True but MS isn’t limited to making money by growing their client’s portfolios; they can just attract new money. It’s the same thing with realtors…the more they sell their client’s houses for the more money they’ll make per transaction but they’ll ultimately make a lot more money by convincing their clients to list their homes cheap so they can sell it quickly and move on to the next listing.

You Wrote: Vanguard funds are rarely, if ever, in the best interests of the client - they are almost exclusively used by people who want a "cheap" fund but don't realize that working with a planner will yield a 2-3% higher return, net of any fees.

I think your definition of “cheap” conflates low cost with low quality. Consider the difference between a Seiko with a simple quartz movement and a Rolex with a fine Swiss movement. The Seiko costs less but it surpasses the Rolex in terms of accuracy, durability, and features. I see this as an excellent analogy to index funds and actively managed funds….one having no moving parts while the other requires a complex mechanism.

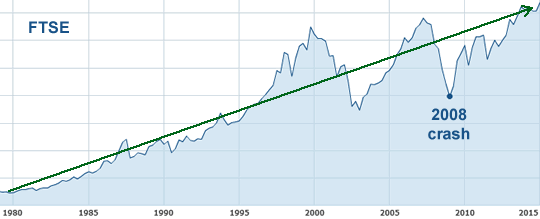

Anyway, my analysis indicates that the large majority of actively managed funds underperform relative to index funds.

The Ph.D. statistician in the “Drunkards Walk” book I recommended tracked the performance of the top 10% of funds managers over time and found that they, as a group, fell to below average performance over time. This strongly suggests that they don’t possess an innate talent, but rather just happened to pick a strategy that worked well for a period of time due to market conditions (Bear Vs Bull market, etc.).

I do believe that a slim few individuals are so talented that they can not only beat the indexes but beat them so hard that they can cover their expenses, salaries, and the additional tax burden they place on their clients due to increased trading but I don’t believe there is a way to identify them soon enough to be of use…basically, by the time you know who they are, they’re retiring.